/

RWA Tokenization in Hong Kong Is Past the Proof of Concept. What Asset Managers Need to Decide Now.

RWA Tokenization

Institutional Markets

RWA Tokenization in Hong Kong Is Past the Proof of Concept. What Asset Managers Need to Decide Now.

Hong Kong's tokenized bond program, Project Ensemble, and its offshore RMB infrastructure define the next phase of institutional RWA tokenization. What asset managers need to decide now.

Roberto Cassa

Marketing Director

How Hong Kong's digital bond program, Project Ensemble, and its position as the world's largest offshore RMB centre define the secondary market and cross-border infrastructure opportunity for institutional investors in 2026

The question that was most frequently asked about real-world asset tokenization in Hong Kong — whether the regulatory and market infrastructure could accommodate it — has been answered. It was answered at sovereign level, in live transactions, across four currencies, and as of November 2025, with settlement denominated in tokenized central bank money. The question that matters in 2026 is different. It is how asset managers and capital markets participants use the infrastructure that has been built, what still needs to be constructed before institutional secondary markets can function at scale, and why Hong Kong's specific position in cross-border capital flows makes its tokenization story fundamentally different from every other major financial centre. Those are architecture questions.

A Proof of Concept That Has Already Run

The HKSAR government's February 2023 issuance of the world's first government tokenized green bond (HK$800 million, one-year tenor, settled on Goldman Sachs' GS DAP platform through the Central Moneymarkets Unit on a T+1 basis) demonstrated that a tokenized bond could settle with statutory finality under Hong Kong law. The February 2024 follow-on, a HK$6 billion equivalent multi-currency offering across HKD, RMB, USD, and EUR tranches settled on HSBC's Orion platform, extended the template to multi-currency issuance and cross-platform interoperability with Euroclear and Clearstream. Both transactions confirmed that the CMU could serve as settlement infrastructure for tokenized debt instruments, with T+1 settlement compressing the timeline that conventional bond issuance processes require.

The November 2025 third issuance moved the story materially forward. At HK$10 billion across four currencies and tenors from two to five years, it was the largest tokenized government bond issued anywhere globally, and the first in the world to integrate tokenized central bank money into the settlement process. Investors settling the HKD and RMB tranches could do so in e-HKD and e-CNY, eliminating traditional counterparty credit risk in settlement and reducing both time and cost in ways that conventional infrastructure cannot replicate. Subscription demand exceeded HK$130 billion, thirteen times the offering size, removing any residual doubt about institutional appetite. The government has now issued three tranches across three consecutive years. The programme is no longer a pilot.

The SFC's November 2023 circular on tokenization of SFC-authorised investment products established the legal basis for private sector participation. The SFC adopted a "see-through" approach: a tokenized instrument is governed by the same regulatory framework as its underlying asset. A tokenized bond is regulated as a bond; a tokenized fund as a fund. The circular also distinguished between tokenized securities (traditional instruments with a digital layer, subject to the same conduct rules as the underlying asset class) and the broader category of digital securities that may exist without a traditional underlying asset, which carry a higher regulatory burden and are treated as complex products by default. That distinction has direct implications for how issuers structure tokenized instruments and for the investor base to which they can be offered.

What Compliant Issuance Requires

For an asset manager or capital markets participant structuring a tokenized instrument in Hong Kong, the regulatory framework is now sufficiently developed to map with reasonable precision. The SFC's see-through principle resolves the product classification question. The choice between a tokenized wrapper and a natively digital structure has operational and legal implications. While native digital instruments currently sit in a less-defined regulatory space and tokenized wrappers inherit the full regulatory treatment of the underlying asset with greater certainty, both approaches are legally permissible and both are subject to the securities framework applicable to the underlying instrument.

The custody dependency is the structural link between the issuance architecture and the compliance analysis set out in this series' previous piece on the incoming VA Custodian Licence. Tokenized securities require regulated safekeeping in precisely the same way as traditional ones, and any institution issuing or holding tokenized instruments in 2026 is doing so in a custody environment that is itself undergoing formal licensing. The question of which entity holds the private keys to tokenized bonds, and under what regulatory obligations, is not merely an operational matter. It is, under the incoming licensing architecture taking shape at LegCo, a compliance question that issuers and institutional holders need to address in their operating model design now.

Project Ensemble, now in its EnsembleTX pilot phase following the November 2025 transition from sandbox to real-value transactions, is the operational environment in which the settlement infrastructure for tokenized instruments is being stress-tested at institutional scale. The pilot involves seven tokenizing banks (HSBC, Standard Chartered (HK), Bank of China (HK), China Construction Bank Asia, Fubon Bank, Fusion Bank, and Bank of East Asia) alongside asset managers BlackRock and Franklin Templeton. The initial use cases are tokenized deposits and tokenized money market fund transactions, but the settlement infrastructure being tested is the same infrastructure that will underpin tokenized bond and RWA settlement at scale: interbank tokenized deposit transfers settled through the HKD Real Time Gross Settlement system, progressively upgrading toward 24/7 settlement in tokenized central bank money. Among the first real-value cross-bank transfers under EnsembleTX was HSBC's HK$3.8 million transfer to Ant International, completed in late 2025, confirming the operational transition from proof of concept to live execution.

The HKMA's Digital Bond Grant Scheme, launched in November 2024, subsidises 50% of eligible expenses for qualifying tokenized bond issuances up to HK$2.5 million per transaction, a direct economic incentive designed to move corporate issuers from observation to execution. The HKMA's August 2023 blueprint on bond tokenization provides the structural template for private sector replication of the sovereign model. More than six corporate entities had issued tokenized bonds in Hong Kong by late 2025, raising a combined USD equivalent exceeding one billion dollars, with Zhuhai Huafa Group's RMB 1.4 billion digital bond among the more significant transactions. The sovereign proof of concept has become a private sector template, and the infrastructure to support it is moving from experimental to institutional.

The Secondary Market Infrastructure Question

The issuance architecture is materially further advanced than the secondary market infrastructure. This gap is not unique to Hong Kong. IOSCO's November 2025 report on the tokenization of financial assets found that market participants across jurisdictions continue to favour traditional settlement infrastructure despite technical capability for on-chain settlement, identifying the absence of high-quality settlement assets on distributed ledger infrastructure and limited cross-chain interoperability as the primary structural barriers. Hong Kong's position is more advanced than most peers, but the secondary market question remains genuinely open.

The November 2025 SFC circular expanding VATP permitted activities introduced the regulatory permission for secondary market trading of tokenized securities on licensed platforms, without applying the twelve-month track record requirement that governs other virtual assets. Licensed VATPs can now distribute tokenized securities and open custody arrangements on behalf of clients. What that circular provides in regulatory permission, the market must now build in operational reality: price discovery mechanisms, liquidity depth, and the interface between VATP-based secondary trading and the traditional clearing infrastructure through which institutional counterparties typically settle their transactions.

HKEX's July 2025 announcement of its Issuer Access Platform, planned for a 2026 launch, and its consultation on reducing the securities settlement cycle from T+2 to T+1, represent the traditional infrastructure side of the same equation. The convergence of a T+1 conventional settlement cycle and a live tokenized securities venue on VATP infrastructure is not yet an integrated operational model. Building that connection is the secondary market infrastructure task that the industry and regulators are both working toward in 2026.

The November 2025 cross-border delivery-versus-payment experiment between Hong Kong's Project Ensemble network and Brazil's Drex central bank digital currency network, conducted via Chainlink's cross-chain interoperability protocol, demonstrated that blockchain-based DVP settlement across jurisdictions is technically achievable. It has not yet become standard market infrastructure, but the experiment demonstrated the feasibility of atomic settlement between on-chain and traditional payment rails, which is the core technical problem that secondary market infrastructure for tokenized RWAs must solve.

The tokenized money market fund launches by ChinaAMC in February 2025 and Franklin Templeton in November 2025 provide the clearest current evidence of what institutional-grade secondary market functionality looks like in practice. Franklin Templeton's fund, settled using HSBC tokenized deposits with 24/7 settlement capability, demonstrates that some of the friction of traditional secondary market infrastructure can be bypassed in specific instrument categories. How that capability extends to a broader range of tokenized RWAs — bonds, private credit, infrastructure assets — is where the secondary market story remains incomplete, and where the operational decisions being made now will define the shape of the market when it matures.

The RMB Gateway Thesis

The question that distinguishes Hong Kong's RWA tokenization narrative from that of Singapore, Luxembourg, or Switzerland is not about regulatory design or settlement efficiency in isolation. It is about capital flows. No other international financial centre combines the world's largest offshore RMB liquidity pool, direct operational integration with China's cross-border wholesale payment infrastructure, and a regulated digital asset framework aligned with both SFC standards and PBOC digital currency settlement initiatives.

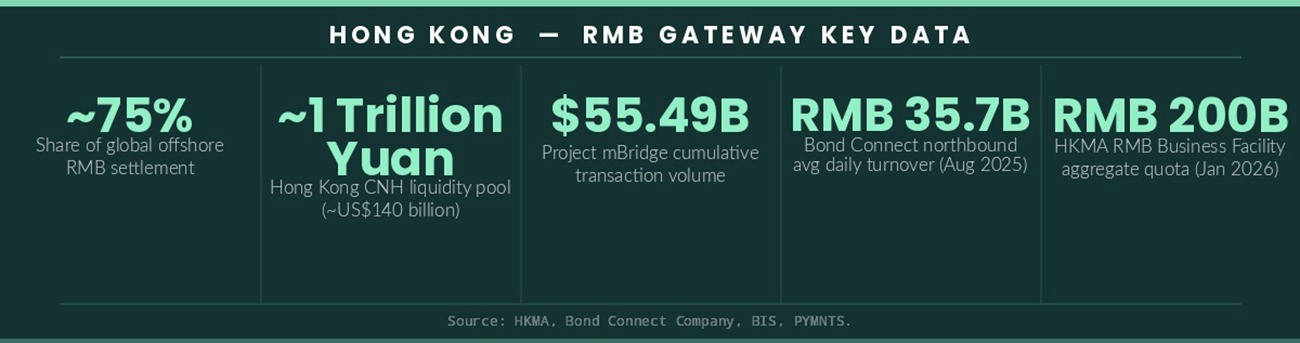

Hong Kong handles approximately 75% of global offshore RMB settlement. The city's CNH liquidity pool stands at approximately 1 trillion yuan (US$140 billion). The HKMA's RMB Business Facility, launched in October 2025 and doubled to a 200 billion RMB aggregate quota in January 2026 after immediate full subscription, reflects the scale of institutional demand for offshore RMB liquidity in the market. Northbound Bond Connect, which operates without quota restrictions for offshore investors accessing China's interbank bond market, recorded average daily turnover of RMB 35.7 billion in August 2025, with repo access under Bond Connect introduced in February 2025 to enable leveraged positions and enhanced liquidity management for offshore investors.

Project mBridge, the multi-CBDC wholesale payment platform involving the HKMA, PBOC, Bank of Thailand, Saudi Central Bank, and Central Bank of the UAE, processed $55.49 billion in 4,047 transactions as of late 2025, with e-CNY representing over 95% of settlement volume. The BIS handed governance of the platform to the participating central banks in October 2024, confirming mBridge's transition from innovation initiative to operational infrastructure. mBridge is not a bilateral pilot between Hong Kong and the mainland. It is the live wholesale cross-border settlement layer connecting Hong Kong's financial infrastructure to the world's second-largest economy's digital currency at scale.

The November 2025 tokenized government bond issuance is the clearest single demonstration of what this integration enables in practice. Settlement of the RMB tranche in e-CNY created the first instance of tokenized CBDC settlement for a sovereign digital bond anywhere in the world, a proof of concept that only Hong Kong could have executed, because only Hong Kong has simultaneous access to e-CNY cross-border infrastructure, HKMA digital bond issuance capability, and institutional investor distribution across global capital markets.

The CMU OmniClear digital bond platform, under construction by the HKMA's subsidiary for a 2026 launch, is designed with regional interoperability as a core requirement from the outset. The platform will connect with tokenization platforms across Asia, beginning with tokenized bonds and progressively extending to other asset categories. Hong Kong is not building a closed digital bond market. It is building the regulated settlement node through which tokenized instruments can move between domestic, regional, and cross-border institutional investors, denominated in CNH, settled in tokenized central bank money, and supported by the most comprehensive digital asset regulatory architecture in the region.

For asset managers evaluating where to build tokenized RWA issuance and distribution capability, the infrastructure argument for Hong Kong is not about regulatory permissibility alone. It is about access. The secondary market for tokenized RWAs that functions at institutional scale in the years ahead will need to reach mainland-connected capital, price in CNH, and settle across the same infrastructure that already handles the bulk of Asia's cross-border capital flows. No other city is in a position to offer that combination.

The Conversation the Market Is Now Having

The feasibility questions have been resolved. The infrastructure questions are now the focus: how compliant issuance connects to secondary market liquidity, how tokenized settlement interfaces with traditional clearing, and how CNH-denominated tokenized instruments access mainland-connected investors through Connect infrastructure. These are questions that institutional participants are working through now, in operating models rather than on paper.

These questions are not answered by regulatory publications alone. They require the direct exchange between issuers, asset managers, custodians, and trading infrastructure providers who share the same compliance obligations but have made different architectural choices. The institutions building Hong Kong's tokenized RWA market in 2026 need a venue where those choices can be examined together, not as competitive positions, but as the operational dependencies of a market still being constructed.

Cosmoverse convenes its Hong Kong Institutional Digital Asset Summit in November 2026, held alongside Hong Kong FinTech Week, as the environment for exactly that conversation. The program's Real-World Asset Tokenization track is built around the infrastructure questions this article has examined: compliant issuance architecture for asset managers, secondary market liquidity and DVP settlement, and the cross-border capital flow thesis that makes Hong Kong's position in tokenized RWA markets distinctive. A closed-door Summit Day provides senior participants from issuers, custodians, trading venues, and asset managers with a dedicated forum for substantive exchange outside the constraints of the main program.

Those looking to engage with the institutions shaping how Hong Kong's tokenized RWA market develops can register at lu.ma/CosmoverseHongKong and explore the broader platform at cosmoverse.org.

Stay informed

Subscribe to the Cosmoverse newsletter to receive Institutional-grade insights on blockchain infrastructure, regulation, and market development.

TAGS

RWA Tokenization

Institutional Markets

Share this article

Key questions addressed in this article

What has Hong Kong done to advance RWA tokenization?

Hong Kong has issued three sovereign tokenized green bonds since February 2023, culminating in a HK$10 billion multi-currency issuance in November 2025 — the largest tokenized government bond globally and the first to settle in tokenized central bank money (e-HKD and e-CNY). The SFC has also established a regulatory framework for tokenized securities using a "see-through" approach, and the HKMA launched Project Ensemble to stress-test institutional settlement infrastructure at scale.

What is Project Ensemble and why does it matter for institutional investors?

Project Ensemble is the HKMA's initiative to build tokenized deposit and settlement infrastructure for institutional use. Now in its EnsembleTX pilot phase with real-value transactions, it involves seven tokenizing banks (including HSBC, Standard Chartered, and Bank of China) alongside asset managers BlackRock and Franklin Templeton. It tests interbank tokenized deposit transfers settled through the HKD Real Time Gross Settlement system, progressively upgrading toward 24/7 settlement in tokenized central bank money.

Why is secondary market infrastructure still a challenge for tokenized RWAs?

While issuance architecture is well advanced, secondary market infrastructure — price discovery, liquidity depth, and the interface between VATP-based trading and traditional clearing — is still being built. The SFC has granted regulatory permission for secondary trading of tokenized securities on licensed platforms, but the operational reality (institutional-grade liquidity and settlement integration) requires further development. HKEX's planned T+1 settlement cycle and its Issuer Access Platform are key pieces of this puzzle.

What makes Hong Kong's position in RWA tokenization unique compared to other financial centres?

Hong Kong combines the world's largest offshore RMB liquidity pool (approximately 75% of global offshore RMB settlement), direct integration with China's cross-border wholesale payment infrastructure via Project mBridge, and a regulated digital asset framework aligned with both SFC standards and PBOC digital currency initiatives. No other international financial centre — including Singapore, Luxembourg, or Switzerland — offers this combination of cross-border capital flow access, CNH pricing, and tokenized CBDC settlement capability.

How does custody regulation affect tokenized securities in Hong Kong?

Tokenized securities require regulated safekeeping in the same way as traditional instruments. Under Hong Kong's incoming VA Custodian Licence framework (currently progressing through LegCo), the question of which entity holds the private keys to tokenized bonds — and under what regulatory obligations — is a compliance requirement that issuers and institutional holders must address in their operating model design now. Custody is the structural link between issuance architecture and regulatory compliance.

Next summit

Get involved, Join the architects of the new financial era.

Hong Kong Institutional Digital Assets Summit

Hong Kong

Tickets

Secure your Seat

Join institutional leaders, regulators, and innovators for the Hong Kong 2026 Summit.

SPEAK

Become a Speaker

Share your expertise on the main stage alongside central bankers and industry pioneers.

Sponsor

Become a Sponsor

Position your brand at the intersection of sovereign technology and institutional capital.